There are three main types of execution venues in the U.S. Equities Market:

Exchanges

Alternative Trading Systems (ATS)

Single Dealer Platforms (SDPs) & Principal Dealers

Trading is either done on exchange (Nasdaq, NYSE, AMEX, etc.) or off-exchange (dark pool or SDP).

Off-Exchange:

Alternative Trading System (ATS) - Also known as “Dark Pools”. These venues allow participants better control over their order and who they are interacting with. Institutions will use an ATS to reduce information leakage (front running of large orders).

Internalization - Using internal books to execute trades. Market Makers will typically internalize flow to minimize risk

Wholesaling - Also known as Payment-for-order-flow, or “PFOF”, is the action of routing retail order flow to market makers who provide execution for the broker’s customers.

.

1. Exchange Venues

There are currently 16 exchanges trading US equities, 24 if you include options exchanges. Exchanges are regulated by the SEC and must be registered with the SEC under Section 6 of the Securities Exchange Act of 1934. Not only are exchanges regulated by the commission, but they are also self-regulatory organizations (SROs) themselves. These exchanges are the primary listing exchanges for most of the world’s largest companies. The US Equities market currently sits at over $44 Trillion in total market capitalization.1

Aside from being the primary listing exchange for stocks, these exchanges also trade in other NMS equity symbols. To incentive trading on their venue, exchanges provide rebates and charge per share fees accordingly.

The Various Pricing Models

Maker-Taker Model

Exchanges generally operate with a Maker-Taker Model. To incentivize trading on their exchange they provide a rebate for an order that adds liquidity (posting orders to their book). When an execution occurs the liquidity provider, Maker, receives a rebate, and the participant who removes that liquidity, the Taker, pays a fee for accessing the liquidity. The exchange makes money on the difference between the removal fee and the adding rebate. Rule 610 of Reg. NMS caps fees at $0.003 per share.2

There has been much debate about the maker-taker model and the impact it may have on market structure and conflicts of interest when brokers handle non-directed customer orders.

Taker-Maker Model

A few exchanges have an inverted maker-taker model. These exchanges offer rebates to participants for removing liquidity from their venue and charge for providing liquidity. These Taker-Maker venues give participants the option to pay to get priority and incentivize other participants to remove that liquidity before venues with other pricing schemes.

`

Flat-Fee Model

These exchanges charge a flat fee for both adding and removing liquidity.

Nasdaq

Nasdaq owns 3 exchanges: the Nasdaq Stock Market, BX (Boston), and PHLX (Philadelphia).3

The Nasdaq Stock Market is a fully electronic stock exchange that has three tiers with unique listing requirements for each. A company must satisfy certain financial, liquidity, and corporate governance requirements to be approved for listing on any of these markets.4 Nasdaq’s Global Select Market has the highest initial listing standard of any exchange. Nasdaq Global Market is for mid & large cap companies with a global reach. Nasdaq Capital Market focuses on companies with smaller market caps with the need to raise capital. The Initial Listing Guide provides detailed requirements for each tier.

Intercontinental Exchange (NYSE)

ICE operates 5 exchanges: the NYSE, American, Arca, Chicago, and NYSE National.

NYSE / NYSE National

The cornerstone of NYSE is the “high touch” Designated Market Maker (DMM). Formerly known as “Specialists”, they have an obligation to maintain a fair and orderly market for the securities they are assigned.

Current DMMS are:

Citadel Securities LLC

GTS Securities, LLC

Virtu Americas LLC

The NYSE has Floor Brokers, who are employees of member firms that execute trades on the floor on behalf of the firm’s clients. As of 2017, there were 205 floor brokers among the 152 NYSE Member Firms (85 Electronic, 5 DMM, 45 Brokerage) on the NYSE.5 Floor brokers act as agents and are physically present on the trading floor. They are heavily involved with opening/closing auctions and NYSE listed IPOs.

The Initial Listing Standards Summary provides the requirements for companies to list on the NYSE.

NYSE Fee Schedule NYSE National Fee Schedule

American (AMEX) - AMEX is the small cap listing exchange for NYSE. It’s a fully electronic price/time priority exchange with a traditional maker-taker fee structure. They also utilize an electronic Designated Market Maker (e-DMMs).

American Initial Listing Standards

Arca - NYSE ARCA is the listing home to many Electronically Traded Products (ETPs) such as SPY 0.00%↑. Arca has a traditional maker-taker fee model and provides a small rebate for midpoint limit orders (MPL).

Chicago (CHX) - NYSE Chicago is a regional exchange that was bought by ICE in 2018. CHX trades in all NMS equity securities except for BRK.A. The regional exchange currently has 30 securities listed on its exchange.

CHX operates on a flat-fee pricing model and only executes a small share of trading volume on a given day (around .25%).

CBOE

The CBOE operates some more unique exchanges. BYX (Formerly BATY), BZX (Formerly BATS), EDGX, and EDGA.

EDGX - Has operated as a fully electronic exchange since 2010. From 2009 through January 2014 both EDGX and EDGA were owned and operated by Direct Edge Holding. in 2013 BATS and Direct Edge announced a merger. In 2016 the CBOE bought BATS for $3.2 billion.

EDGX offers trading in all U.S. listed equities.

Display-Price Sliding: An order instruction where if an order would be locking/crossing an external market the order will maintain its time priority in the queue at one minimum price increment higher/lower.

In 2015, the SEC fined Direct Edge exchanges for failing to properly describe three sliding order types, Hide Not Slide, Price Adjust, and Single Re-Price. In the SEC complaint, the regulators alleged that a high frequency trading firm, who was a subscriber of the Direct Edge ECNs, was running a trading strategy that was designed to capture spreads and collect rebates offered by the trading centers for providing liquidity.

The problem with the EDGX order was then the orders un-slid, they would receive a new timestamp at the previously locked price and occasionally end up removing liquidity.

The HFT firm requested an alternative price-sliding function that would allow an otherwise locking/crossing order to “hide” and maintain its rank and be executable and Hide Not Slide was born. If the NBBO changed where the original order price could be displayed without locking/crossing a protected quote, EDGX would unhide the order at its original rank in their order book without applying a new timestamp. This HNS order would have execution priority over the default price sliding functionality.

EDGA - EDGA is an all electronic exchange with a low cost flat-fee model. They used to operate with a taker-maker model, but that changed in May of 2017.

BZX - Formerly known as BATS, this exchange has a flat-fee pricing model. The original name was Better Alternative Trading System (BATS) and initially operated as an ATS. Bats Global Markets became a registered exchange in 2008 and launched BYX in 2010.

BYX - Formerly known as BATY, BYX has a taker-maker pricing model. BATY currently operates with about a __% share of trading volume

IEX

IEX was the focus of Michael Lewis’s book, Flash Boys. IEX utilizes a “speed bump”, which is a 38-mile long coiled cable that all incoming orders go through before reaching their matching engine. This physical speed bump creates a 350-microsecond delay which prevents market participants from having a speed advantage over the exchange. The primary benefit of this speed bump is that it prevents latency arb traders from picking off stale pegged orders.

In 2020 the SEC approved a new order type proposed by IED called D-Limit, an optional order type that utilizes an algorithm called the “Crumbling Quote Indicator”). The CQI takes real-time data from multiple exchanges to predict when the NBBO is likely to change in the next two milliseconds.6 If the CQI determines the NBBO is “crumbling”, this order type will automatically re-price one increment. These two-millisecond time increments total on average five to ten seconds each trading day.

Member’s Exchange (MEMX)

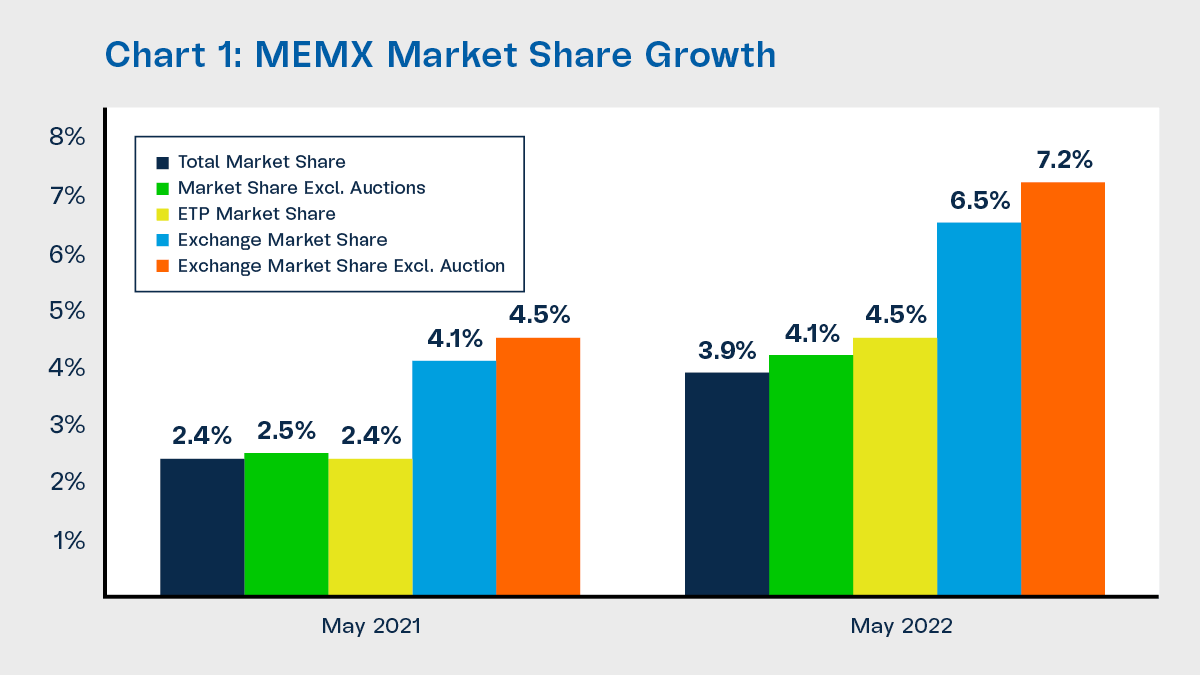

The Member’s Exchange is owned by a consortium of 17 different institutions, MEMX represents the interests of its members and their collective client base, comprised of retail and institutional investors, on U.S. market structure issues.7 The Members Exchange went live with their first trade on September 21, 2020 at 7:48:43 AM executing 100 shares of ED 0.00%↑ at $73.90. Through the first day of trading 25 firms traded a total of 60,957 shares.8

MEMX entered the market with a juicy rebate structure, particularly for retail orders — Retail orders adding liquidity on MEMX currently receive $0.0035/share. These rebates have led to great market share growth for the new exchange in 2020 and 2021 as the retail trading craze dominated lower-priced stocks. In May 2022, MEMX’s exchange market share excluding auctions was 7.2%, a 60% increase YoY. Looking at exchange share by tape, MEMX was ranked the 5th largest exchange in Tape B and Tape C and the 6th largest exchange in Tape A.9

Long-Term Stock Exchange (LTSE)

The idea of the LTSE was first introduced back in 2011 in Eric Ries’s book The Lean Startup. Eric founded the LTSE in 2015 and officially opened for business in September 2020.

The idea of the LTSE is to promote long-term, each company listed on the exchange is required to adopt and publish five long-term policies covering its long-term strategies, practices, and plans for stakeholders and shareholders.

For trading, the LTSE does not pay or charge for market participants to interact on their exchange. Orders are simple (Limit & Market), with price/time priority and exclusively displayed.

Miami International (MIAX)

Miami International operates 3 exchanges, MIAX, Pearl, and emerald. They have a market share in options trading of ~13.8% and an equities trading market share of 0.92%

MIAX Pearl Equities supports RHO, IOC Limit orders, display and non-displayed, ISO, minimum execution quantity orders, reserve orders, and attributions. MIAX Pearl Equities also offers the following routing strategies:10

Order Protection: Order Protection is a routing strategy under which an order checks the Pearl Equities order book for available shares and then is routed to attempt to execute against Protected Quotations at away Trading Centers. All routable orders will default to the Order Protection routing strategy.

Route to Primary Auction (“PAC”): PAC is a routing strategy for Market Orders and displayed Limit Orders designated as RHO that the entering firm wishes to designate for participation in the opening, re-opening (following a regulatory halt, suspension, or pause), or closing process of a primary listing market (Cboe BZX, NYSE, Nasdaq, NYSE American, or NYSE Arca) if received before the opening, re-opening, or closing process of such market. The System will designate such orders routed pursuant to the PAC routing strategy with the time in force accepted by the primary listing market. Displayed Limit Orders coupled with the PAC routing strategy will be eligible to be routed pursuant to the PI routing strategy described directly below when resting on the MIAX Pearl Equities orderbook in continuous trading.

Price Improvement (“PI”). PI is a routing strategy that will route a displayed Limit Order coupled with the PAC routing strategy to multiple destinations simultaneously at a single price level. PI is not an independent routing strategy and may not be selected individually upon order entry.

The standard rates for securities above $1.00 is ($0.0029) per share for adding displayed liquidity, and a rebate of ($0.0021) for adding non-displayed liquidity, and a fee of $0.0029 for removing liquidity.

2. Alternative Trading Systems

Also known as “Dark Pools”, off-exchange venues come in many forms. Broker-Dealers do a variety of business for a wide range of clients and need the ability to achieve best execution for them.

All trades in these venues print to the tape as off-exchange and are reported to NASDAQ/FINRA’s Trade Reporting Facility (TRF). When you see “FINR” or “FINRA” in your prints, those trade printed “Off-Exchange”.

Many ATSs are operated by multi-service broker-dealers. These BDs can leverage their ATSs to complement other offerings to their subscribers. For instance, a broker-dealer may run a market-making desk or execute principal trades and use their ATS as an opportunity to execute orders before seeking a contra party at another trading center.

Rule 300(a) defines an ATS as:

"any organization, association, person, group of persons, or system: (1) [t]hat constitutes, maintains, or provides a market place or facilities for bringing together purchasers and sellers of securities or for otherwise performing with respect to securities the functions commonly performed by a stock exchange within the meaning of [Rule 3b-16]; and (2) [t]hat does not: (i) [s]et rules governing the conduct of subscribers other than the conduct of such subscribers’ trading on such organization, association, person, group of persons, or system; or (ii) [d]iscipline subscribers other than by exclusion from trading.”

All ATSs must be run by registered Broker-Dealers and must file Form ATS-N with the SEC.

Virtually all ATS operators utilize a Smart Order Router (SOR) to route orders among a variety of trading venues, typically these routing algos include additional ATSs not owned by the operator and will even post liquidity on an exchange if no liquidity is found.

Today there are over 30 ATSs operating, in 2002 there were less than 10 ATSs. The growth in ATSs has caused a massive fragmentation of liquidity in the marketplace, but these alternative trading venues provide immense value to participants. The anti-gaming safe measures provided by ATSs gives institutions safeguards against frontrunning their large orders. For traders, one of the key advantages of trading in an ATS is the ability to execute at sub-penny increments on stocks over one dollar.

The reason Alternative Trading Systems have taken such a substantial percentage of trading volume is that they have unique models when compared to the standard price-time priority that exchanges offer — like price/capacity/size/priority/interval.

The Barclays ATS LX

LX is a non-displayed ATS that uses a price-tier-time priority for execution. The tiers give priority to Barclays institutional clients and Algo/Router users. The tier structure is only used for subscribers who are adding liquidity.

Barclays employs a framework called Liquidity Profiling for categorizing liquidity removing activity within our ATS.

Liquidity Profiling categorization applies only to Subscribers that route directly to LX when removing liquidity, and is based on one-second alpha, which is the midpoint-to-midpoint market movement over a one-second horizon, normalized by the daily average spread.

Based on this metric, Subscribers are placed into one of three alpha categories: Low, Medium, and High (Low being the lowest alpha category <0.141 and High being the highest alpha category >0.201). Barclays reserves the right to review and adjust the factors considered when categorizing Subscribers based on their order flow that removes liquidity. Orders routed to LX by the Router or the Algos are placed into the Low alpha category by default

Barclays also provides detailed reports to their clients that provides a variety of information regarding the customer’s orders; execution venues, percentage of order flow executed in various venues, crossing rates with the Barclay’s ATS, and the percentage of order flow executed against the various types of counterparties trading within LX.

Subscribers of this ATS can customize how their orders interact within LX:

Counterparty Restrictions: Restrict interaction with certain Subscribers or Subscriber types, or liquidity profiling category

Conditional order

Minimum quantity

Blocking principal orders

Restricting by minimum duration

3. Single Dealer Platforms & Wholesalers

Single Dealer Platforms (“SDP”) are exactly what they sound like. Rather than going to an exchange or ATS where they match your trade with another participant, an SDP is a platform owned and operated by a member, and that member trades solely for their own account. Orders routed to an SDP that are marked as immediate-or-cancel (“IOC”) or fill-or-kill (“FOK”) are either filled on a principal-only basis or canceled.

Transactions that occur on SDPs are considered off-exchange and are reported to the Trade Reporting Facility (TRF).

Virtu, Jane Street, IMC, Citadel, Barclays, and Hudson River Trading all operate SDPs.

Wholesalers

Wholesale Market Makers who execute retail orders. Principal dealers have exploded in recent years thanks in large part to Robinhood’s disruptive business model in the retail brokerage space. The wholesalers provide retail customers with executions at or better than the National Best Bid or Offer “NBBO”.

SEC Rule 606 requires brokers to make publicly available a quarterly report regarding their routing of non-directed orders. They must also disclose Payment for Order Flow “PFOF” practices pursuant to SEC Rule 607.

Robinhood 606 & 607 Disclosure

Typically, the payment received by retail brokerages is a payment based upon a fixed percentage of the spread between the National Best Bid and the National Best Offer at the time of execution. At Robinhood, each market maker pays the same rate, so they are not incentivized to send flow to any one specific market maker. Instead, each retail broker determines where they send their order flow through a proprietary routing system. These firms have a set of benchmarks to measure the quality of price improvement of various wholesalers and send flow accordingly.

Retail Volume

According to Rule 605 Reports from wholesalers, in 2020 retail volume accounted for 21% of the total market volume traded in US equities. Of that, 14% was posted, 26% routed, and 60% executed with wholesalers.11

Virtu says approximately 40% of total retail flow handled by them interacts with liquidity on public exchanges or ATSs while 60% is internalized within Virtu (this could be in a riskless principal or principal transaction).

Summary

With the fragmentation in the U.S. Equities Market it is important to know the venues and how participants interact with them. Understanding fee schedules and offerings of various trading venues can give you context on how to reduce trading costs and increase fill rates.

Additional Topics

The next chapters of this series will be a summary of the debate on PFOF, shedding light on dark pools, and the history of ECNs.