Debunking Ape Theory

Clarifying some common misbeliefs among apes about short selling, clearing & settlement, and fail-to-delivers.

Before you read this article, I have grossly simplified a lot of information here for the sake of saving time. A lot of these processes are extremely complex, and I am actively trading as I write this, so if you notice an error or think these thoughts are all over the place just remember I was probably getting destroyed in a position. :)

Since all of this has unfolded, I have read and commented on some hilariously horrible takes from people using hashtags like #ApeStrong #AMCARMY #AMCAPES, I watched Trey spewing false narratives to his YouTube audience and read some Redditor’s half baked “due diligence”— which is more akin to a conspiracy theory than actionable research.

The tipping point for me was when I watched this viral clip from Joe Rogan’s recent podcast episode, with his guest Adam Curry regurgitating some of the same ridiculous takes being touted by the apes.

“If you look at the DTCC, it’s the clearing house, there’s probably a thousand times more shares of every company that is traded than actually exist. It’s all in the system, it’s all fucking bullshit options.” — Adam Curry, JRE #1679

Short Selling: The Basics

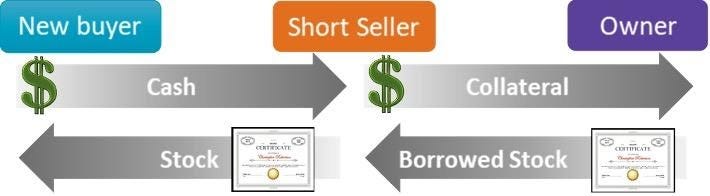

Trader A is long 100 shares and lends them to me to short, I borrow the shares from Trader A and sell them to Trader B. While both Trader A and Trader B are long the same shares, Trade A has agreed to lend those shares with rights: voting right, right to dividends, and special payments from the company.

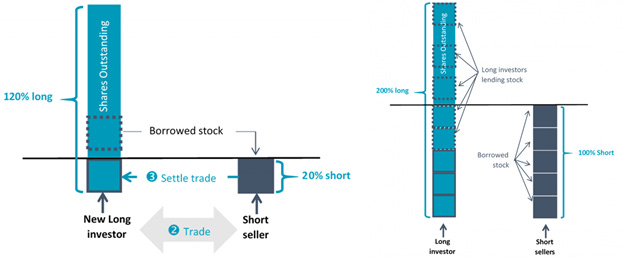

Short positions can only be established when they trade with a buyer. The buyers are increasing long exposure at the same rate that short sellers are increasing exposure, if a stock is 100% short then there is an equal amount of additional long exposure on the other side. 1

Market mechanics such as the Uptick Rule (SEC Rule 201) prevents short-sellers from accelerating downward momentum, by hitting the bid, in securities that are down more than 10% in a day and requires short positions to be filled on an uptick — which means a buyer has to be willing to pay for the price that the short seller is offering. As soon as a stock trades -10 percent on the day, the uptick rule is in effect for the remainder of the day and all of the following day.

Ape Myth: Short selling can put a company into bankruptcy.

Truth: The stock price has almost nothing to do with the underlying company’s financials and ability to meet obligations. Short selling does not cause bankruptcy, it’s just a way to profit from a security going down in price. Companies go public for access to capital or for investors to profit. As long as there is an appetite from investors, a publically traded company could issue new shares and raise capital to meet obligations, but at the cost of diluting the equity for existing shareholders.

Securities Lending

Securities Lending is a complex process that facilitates asset redistribution within the financial markets. More precisely, securities lending is the market practice by which securities are transferred temporarily from one party, a securities lender, to another, a securities borrower, for a fee. This transfer is secured by collateral, which can be cash or another security. 2

Securities lenders are often pension funds, sovereign wealth funds, mutual funds, insurance companies, and ETFs who are interested in earning incremental income on their idle assets.

Borrowers are typically Hedge Funds, Mortgage REITs, and Broker-Dealers whose motivation is to facilitate their trading activity, typically various arbitrage strategies or market-making.

A borrower is obligated to make equivalent payments of any dividend or distribution to the lender who would have received it had they not lend out the shares. Most agreements allow the lender the ability to recall shares on loan at any time — usually if they want to participate in a vote or close their position. If a short seller’s borrowed shares get recalled and they wish to remain short, they would either have to secure a borrow for delivery— or get bought in.

Counterfeit Shares are NEVER Created

Any time a short position is taken a new long position is also created on the other side of the trade, the transaction nets out, and no new shares are created.

The term securities lending is actually misleading. The transaction is technically a transfer of title that is fully collateralized by the borrower. It is essentially a sale where the seller can reclaim possession whenever the agreement allows. This obligation, or IOU, allows idle assets to be freely traded which improves liquidity and price discovery in the market. Although the lender technically no longer owns the shares, the exposure of those shares still exists on their books.

Ape Myth: Hedge Funds engage in massive naked short selling to suppress stock prices

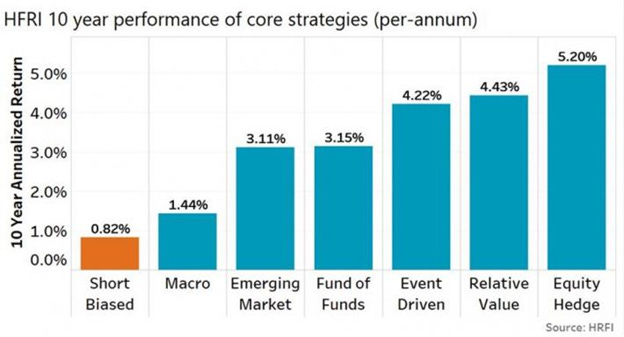

Truth: Short-biased hedge funds consistently underperform other types of funds. Improvements to Reg SHO have made naked short-selling low-hanging fruit for FINRA to enforce. Most of these Reg SHO violations stem from inadvertent system failures rather than market manipulation.

Trade Settlement

Settlement occurs when the purchase is funded and the shares are delivered to the purchaser. The regular way settlement cycle for US equities is two business days after the trade date or T+2.

The vast majority of customer stock is held in street name, which means securities are held in the name of the brokerage firm in the central depository trust (DTC). Because of this, corporations do not know the names and addresses of their shareholders. Under SEC Rule 14b-1, issuers may request investor information from Broker-dealers holding stock in street name. Customers may object to the release of such information and instead can opt for the broker-dealer to forward the information to them.

What is the DTCC?

The Depository Trust & Clearing Corporation, or DTCC, is the central clearinghouse for all the other clearing firms; they act as the intermediary between members. These members are either Prime Brokers or self-clearing Broker-dealers (BDs). The DTCC operates many subsidiaries, the DTC and NSCC are the main two regarding equities settlement. The DTCC operates three subsidiaries that are designated as Systemically Important Financial Market Utility (“SIFMU”) under Title VIII of Dodd-Frank, both the DTC and NSCC are designated SIFMUs and regulated by the SEC. The NSCC is also known as a Central Counterparty Clearinghouse or CCP.

The NSCC operates two core systems:

1)Universal Trade Capture (UTC)

This is the first step in the clearing and settlement process. Daily Receipts of trade data from over 50 venues, exchanges, ATS, and NSCC members are compared and validated. Over 94% of trade data is submitted “locked-in” meaning it has already been compared by the marketplace of execution.

2)Continuous Net Settlement (CNS)

All eligible and compared transactions for a particular settlement date are netted into either a net debit or net credit position for each member. To reduce counterparty risk, the DTCC then becomes the central counterparty to these netted positions and guarantees that every trade will eventually settle, even if the original buyer/seller defaults.

This multilateral netting process reduces the total dollar value of trades that will be settled by an average of 98 percent each settlement day. As the DTCC says in a blog post, “To illustrate, over a 28-day sample in November and December 2018, the average gross settlement balance was $326 billion, and the net was $32 billion, 90% of the funding needs were eliminated via netting”.

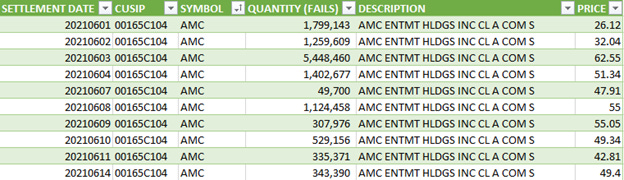

Fail-To-Deliver (FTDs) Reports are the best empirical evidence that naked short selling is not rampant.

FTD data comes in a text file that contains a CUSIP number, ticker symbol, issuer name, price, and a total number of fails-to-deliver (i.e., the balance level outstanding) recorded in the Nation Securities Clearing Corporation’s, or NSCC, Continuous Net Settlement (CNS) system aggregated over all NSCC members.

A failure to deliver occurs when a broker-dealer fails to deliver securities to the party on the other side of the transaction on the settlement date. There are many justifiable reasons why broker-dealers do not or cannot deliver securities on the settlement date. A broker-dealer may experience a problem that is either unanticipated or is out of its control, such as

delays in customers delivering their shares to a broker-dealer,

the inability to obtain borrowed shares in time for settlement,

issues related to the physical transfer of securities, or

the failure of a broker-dealer to receive shares it had purchased to fulfill its delivery obligations. Failures to deliver can result from both long and short sales.3

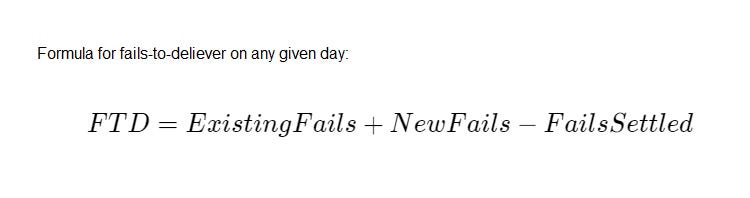

The SEC says failures to deliver on a given day are a cumulative number of all fails outstanding until that day, plus new fails that occur that day less fails that settle that day. The figure is not a daily amount of fails, but a combined figure that includes both new fails on the reporting day as well as existing fails. In other words, these numbers reflect aggregate fails as of a specific point in time and may have little or no relationship to yesterday's aggregate fails. 4

The recent ape theory is that FTD data is the key for timing short squeezes based on Reg SHO closeout requirements. But that theory completely neglects that the daily quantity reported is an aggregate of existing and new fails. AMC was trading on average half a billion shares per day, even an aggregate of 5 million fails would not cause a short squeeze.

Another theory I read is that traders can “reset the clock” on a firm’s Reg SHO close-out requirement by using options. This trading practice is illegal and the takeaway from a previous ruling in 2016, is that broker-dealers have an obligation to monitor for, and prevent, this type of trading by their customers. Failure to do so will result in disgorgement and penalty fines for the BDs.

Reg SHO

Regulation SHO creates rules and uniform standards regarding short sales. The regulation applies to equities and any security that is convertible into equities.

Reg SHO provides market makers an exemption from pre-borrowing shares before shorting, market makers are NOT exempt from borrowing shares completely. The reason this exemption is in place is that market-makers have an obligation to maintain a two-sided market — failure to honor these quotes for the minimum quote size is known as “backing away” and is a violation of the Firm Quote Rule (SEC Rule 11Ac1-1). Special and even exclusive arrangements with securities lenders allow market makers the ability to secure borrows to facilitate an orderly market.

Rule 204, also known as the closeout requirement, reduces the number of FTD positions by requiring broker-dealers that have a fail-to-deliver position to either; immediately purchase or borrow the security to close out the fail. No short sales on that security are permitted by the BD (or any BD that the firm clears for) unless it has arranged to borrow the securities. An exception exists for bona fide market-making activities and the broker-dealer gets an extra two settlement days.

Options Trading Volume

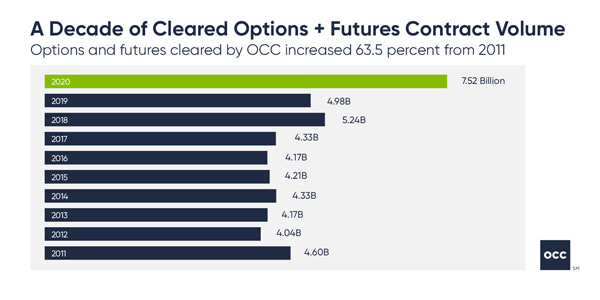

The rise of retail trading interest from work-from-home boredom coupled with free trading thanks to the rise in Payment For Order Flow (PFOF), and the ease of access to options trading has led to an insane increase in derivative trading volumes. According to the OCC, full-year cleared contract volume in 2020 was up a staggering 50.6 percent from 2019.5 So far in 2021, total equity options volume is up an additional 47.5 percent from 2020’s elevated levels! Interestingly, both Index Options and Futures trading volume is down around -15% YoY.

Retail traders are attracted to options because they provide a sort of synthetic leverage for their relatively small accounts and a safe harbor from the Pattern Day Trading (PDT) rule. This huge increase in options trading volume has created an interesting and almost perplexing level of trading in the respective underlying assets, adding a whole new dynamic to the markets.

Conclusion

Like every “fun” conspiracy theory, there is an ounce of truth. There is no doubt manipulation in the markets that exist today on every level — dilution scams, pump-and-dump schemes, bogus press releases, fake bids, layering, painting the tape, and so on do exist — after all, the people at FINRA and the SEC still have jobs.

If you have any questions please check out some of the sources that I linked below or message me on Twitter. I plan on writing more of these so if you enjoyed this newsletter and want to learn more about the markets then get subscribed (its free).

https://www.nasdaq.com/articles/how-short-selling-works-2021-02-04

https://www.econstor.eu/bitstream/10419/130648/1/835456919.pdf

https://www.sec.gov/data/foiadocsfailsdatahtm

https://mondovisione.com/media-and-resources/news/occ-clears-record-setting-752-billion-total-contracts-in-2020-december-volume/#:~:text=Options%3A%20Total%20exchange%2Dlisted%20options,up%2058.5%20percent%20from%202019